Filing Your Final Capital Stock/Foreign Franchise Tax Report

The Capital Stock/Foreign Franchise Tax has expired for tax years beginning after December 31, 2015. With its expiration, corporations will need to re-evaluate their RCT-101 filing requirements. Corporations that annually file the RCT-101 to report only Capital Stock/Foreign Franchise Tax will not have an annual filing requirement for tax years beginning after December 31, 2015. Such corporations should file a final RCT-101 for their 2015 reporting period. For calendar year filers the final tax filing year is tax year ending December 31, 2015. The final tax year for fiscal filers includes those tax years beginning in 2015 and ending in 2016.

The PA Corporate Tax Report (RCT-101) is due annually on April 15 of the year following the year for which the report is submitted for a calendar year reporting corporation, or 30 days after the federal due date for corporations reporting to the federal government on a fiscal year basis. Domestic International Sales Companies (DISC) must file on or before the 15th day of the 10th month following the close of the fiscal year.

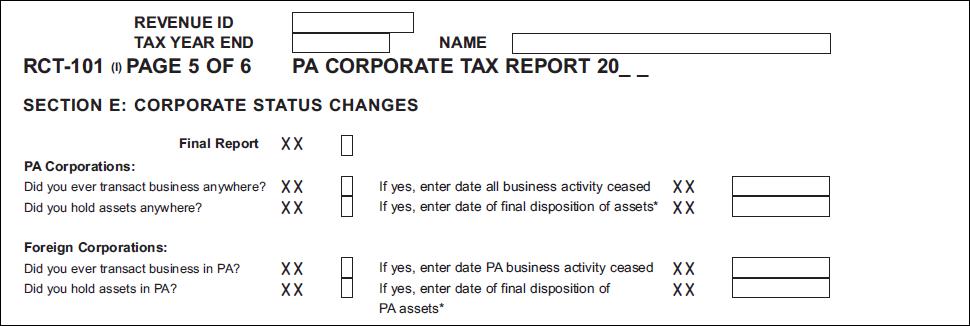

The Bureau of Corporation Taxes is requesting that all taxpayers only subject to Capital Stock/Foreign Franchise Tax identify their 2015 return as their “final report” by checking the indicator box on page 5 of the return under Section E: Corporate Status Changes. In addition, the Bureau of Corporation Taxes is requesting a statement accompany the final RCT-101 filing stating the entity is no longer subject to the Capital Stock/Foreign Franchise Tax.

This means that entities that are not subject to the Corporate Net Income Tax will not have a RCT-101 filing requirement and can be closed. These entities include: single member LLC’s, Multi Member LLC’s taxed as a partnership or S Corporation, S Corporations, and Business Trusts that are not federally taxed as a C corporation. Solicitation only corporations would also no longer be required to file the RCT-101.

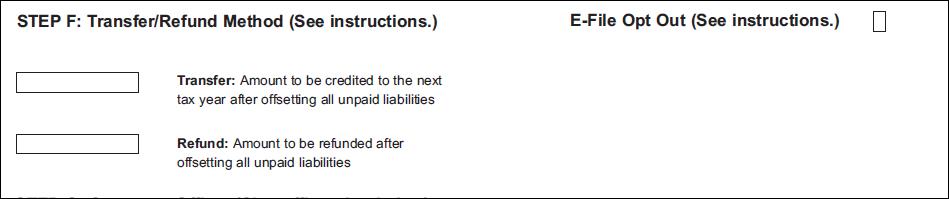

Important: Complete Step F on Page 1 of the RCT-101 if you have an overpayment that needs refunded or transferred to another tax.

Taxpayers who, in addition to no longer being subject to Capital Stock/Foreign Franchise Tax, intend to go out of existence and close their corporate charter will also need to file the REV-181 (Application For Tax Clearance Certificate) to close their charter with the Department of State. Simply checking the “Final Report” box on the RCT-101 will not close the account with the Department of State.